A working adult earning $48,000 per year, eligible for partial Pell Grant, with $5,250 in annual employer tuition reimbursement, can complete a bachelor’s degree at $350-per-credit online programs with approximately $4,200 in total out-of-pocket cost over 4 years. The same person without benefit stacking would pay $42,000. The difference, roughly $37,800, is not from a single program or institution. It comes from understanding how three federal-law-defined education benefits combine, in what order they apply, and how to pace coursework to capture the maximum stacked value.

This guide breaks down exactly how Section 127 employer tuition reimbursement stacks with Pell Grant, GI Bill, and transfer credits to produce real out-of-pocket savings for working adults pursuing online degrees. It includes a calculator that lets you input your specific situation and see your stacked benefit position immediately, along with the strategic framework for maximizing what you receive.

Section 127 Tuition Stacking Calculator

See how employer tuition reimbursement, Pell Grant, GI Bill benefits, and transfer credits actually stack to reduce your real out-of-pocket cost for an accredited online degree.

Your stacked benefits

Updated automatically as you change inputs above.

Find programs that match your stacked benefits

Now that you know your real out-of-pocket cost, explore accredited online programs that fit your budget, timeline, and career goals.

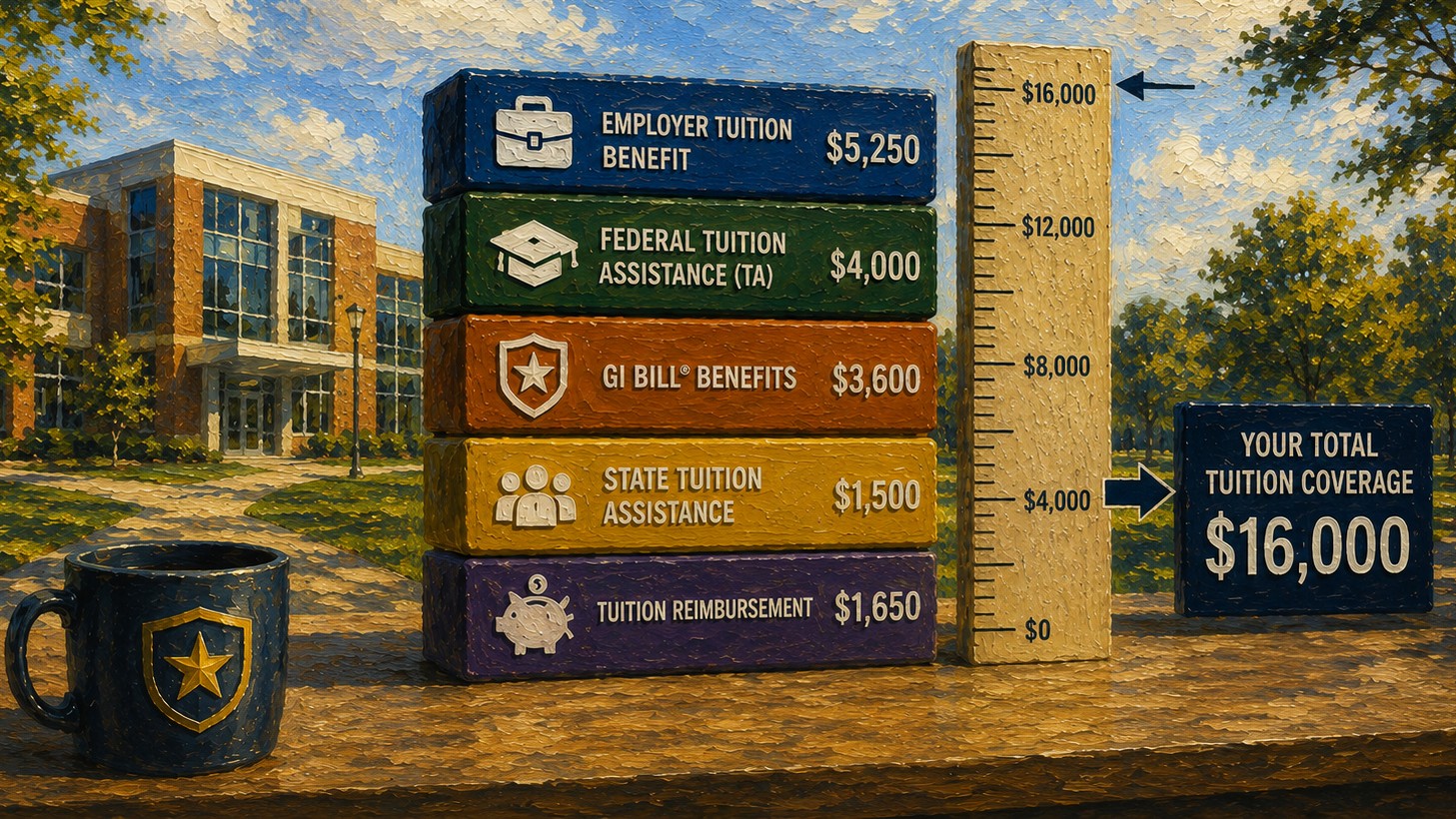

See Best-Fit ProgramsSection 127: Internal Revenue Code Section 127 allows employers to provide up to $5,250 per calendar year in tax-free educational assistance. Amounts above $5,250 are taxable to the employee. This calculator assumes annual reimbursement is paid in full to the cap each year of the program.

Pell Grant: The 2025-2026 maximum Pell Grant is approximately $7,395. Eligibility is based on Expected Family Contribution from FAFSA. This calculator assumes full Pell eligibility for the full duration of the program; actual eligibility can change year-over-year based on income.

GI Bill and military benefits: Actual benefits depend on service eligibility, percentage of benefit earned, institution type (public vs. private), and Yellow Ribbon Program participation. Verify your specific entitlement at va.gov/education before relying on these estimates.

What this calculator does not capture: Books and fees (typically $1,000-$2,500 per year above tuition), state-specific aid programs, scholarships, employer service commitments (some employers require continued employment after reimbursement), tax implications of reimbursement above $5,250, and tuition increases during program duration.

Verification recommended: Confirm specific benefit amounts and eligibility with your employer HR department, FAFSA at studentaid.gov, and VA education benefits office before financial planning. This calculator provides estimates for planning purposes only.

For the broader foundation on accredited online degrees as an adult learner: The Complete Guide to Earning an Accredited Online Degree as an Adult Learner.

What Section 127 Actually Is (And Why It Counts)

Internal Revenue Code Section 127 is the federal law that allows employers to provide up to $5,250 per calendar year in educational assistance to employees on a tax-free basis. IRS Publication 970 documents the rules. The benefit covers tuition, fees, books, and supplies for both undergraduate and graduate coursework at accredited institutions.

Three specific facts about Section 127 affect how working adults should plan around it:

- The $5,250 cap is per calendar year, not per academic year. The cap resets every January 1, meaning a single academic year can capture two calendar years of benefit if courses span the calendar boundary.

- Amounts above $5,250 in a single calendar year are taxable to the employee. Some employers (Boeing, Verizon, RTX, Bank of America) provide reimbursement above the cap; these amounts add to your W-2 taxable income and increase your tax liability accordingly.

- The reimbursement is tax-free to the employee, not deductible separately. You do not file additional paperwork to claim the benefit; the employer’s payment satisfies the obligation directly.

For employees at companies offering the standard $5,250 cap, this works out to approximately $437.50 per month in tax-free educational benefit. Over a 4-year bachelor’s program, that totals $21,000 in employer contribution. For employees at companies offering more (Boeing’s $25,000 annually, Verizon’s $13,250, RTX’s no-cap Employee Scholar Program), the totals are substantially higher.

For the broader employer tuition reimbursement framework: Employer Tuition Reimbursement Explained.

What Stacks With Section 127 Reimbursement

Section 127 employer reimbursement is one of four benefit categories that working adults can combine to reduce online degree cost. Each operates under different rules and applies to different portions of the total cost. Understanding the stacking order matters because some benefits cap based on remaining cost after other benefits apply.

Pell Grant (Federal Need-Based Aid)

The Pell Grant is federal need-based financial aid that does not require repayment. Pell Grant Overview documents that the maximum award for 2025-2026 is approximately $7,395 per academic year, with partial awards ranging from $750 to $5,000 for students with moderate financial need.

Eligibility is determined through FAFSA based on Expected Family Contribution. Working adults often miss Pell Grant eligibility because they assume need-based aid is for traditional-age students. In reality, a working adult earning $45,000 to $55,000 (depending on family size and household composition) typically qualifies for partial Pell. A worker with dependents earning $60,000 to $70,000 may still qualify for partial awards.

Pell Grant stacks with Section 127 reimbursement. The two benefits apply to different portions of the cost: employer reimbursement applies first (typically capped at the federal $5,250), Pell Grant applies to remaining cost. If the combination exceeds tuition cost, excess Pell Grant funds can be applied to books, fees, transportation, and living expenses.

For the complete FAFSA process for online students: FAFSA for Online Students.

GI Bill and Military Tuition Benefits

Military service members, veterans, and military families have access to several education benefits that stack with Section 127 reimbursement:

- Post-9/11 GI Bill (Chapter 33): pays tuition and fees up to the highest in-state undergraduate rate at public institutions, with additional Yellow Ribbon Program participation at private institutions

- Montgomery GI Bill: provides a fixed monthly stipend for education

- Military Tuition Assistance (TA): active-duty service members can receive up to $250 per credit hour and $4,500 per fiscal year

- MyCAA Scholarship: military spouses of E-5 and below ranks can receive up to $4,000 lifetime for portable career credentials

- VA Vocational Rehabilitation (Chapter 31): service-connected disabled veterans receive tuition, fees, books, and monthly stipend

For the GI Bill vs Military TA decision: GI Bill vs Military Tuition Assistance: Which Should You Use First?.

For complete military TA strategy: How to Use Military Tuition Assistance (TA) for an Online Degree (2026).

Verify current benefit amounts and eligibility at VA Education Benefits.

Transfer Credits (Effectively Free Reduction of Total Cost)

Transfer credits are the most underutilized cost-reduction mechanism for working adults. Every accepted transfer credit eliminates a credit you would otherwise pay for. Working adults frequently have substantial prior coursework, military experience, or industry certifications that translate to college credit through transfer evaluation or prior learning assessment.

Common transfer credit sources for working adults:

- Prior college coursework, even if from many years ago (most institutions accept transfer credits with no time limit on general education courses)

- Military training and occupational specialties (American Council on Education’s Military Evaluations program translates military training to college credit)

- CLEP examinations (College-Level Examination Program): pass an examination, earn credit equivalent to a college course

- Sophia Learning, Study.com, and similar online course providers offer credit-bearing courses at $79-99 each that transfer to many institutions

- Industry certifications (AWS, Cisco, CompTIA, PMP, SHRM, others) translate to credit at institutions with prior learning assessment programs

For the institutions with the strongest transfer credit acceptance: Best Online Universities With Generous Transfer Credit Policies.

A working adult entering a 120-credit bachelor’s program with 30 transfer credits effectively reduces the program to 90 credits. At $350 per credit, that’s $10,500 in eliminated cost before any employer or federal aid applies.

How Benefits Actually Stack: The Order Counts

Benefits apply in a specific order that affects the total amount each contributes. Understanding the stacking order is important because some benefits cap based on remaining cost after other benefits apply.

Step 1: Reduce Total Credits Through Transfer

Transfer credit acceptance happens before any tuition is paid. The result is a smaller total number of credits required, which reduces total program cost proportionally.

Example: A 120-credit bachelor’s at $350 per credit costs $42,000. With 30 transfer credits accepted, the program drops to 90 credits, costing $31,500. That’s a $10,500 reduction before any other benefit applies.

Step 2: Apply Employer Reimbursement

Employer reimbursement under Section 127 applies to tuition costs as you pay them. The employer typically requires you to pay upfront, complete the course, then submit documentation for reimbursement. The reimbursement is capped at $5,250 per calendar year (or whatever your specific employer’s policy permits).

Example continued: At 90 credits remaining and 15 credits per year, the program takes 6 calendar years. At $5,250 per year for 6 years, employer reimbursement totals $31,500, which exactly covers the remaining tuition. Out-of-pocket cost: $0.

This is why employer reimbursement is the foundation of stacking strategy. At appropriate per-credit pricing and pacing, employer reimbursement alone can fully fund a degree.

Step 3: Apply Pell Grant

Pell Grant applies to remaining cost after employer reimbursement. If employer reimbursement covers all tuition, Pell Grant excess can apply to books, fees, transportation, dependent care, and other education-related expenses.

Example continued: If our worker also qualifies for $3,500 annual Pell Grant, the $3,500 × 6 years = $21,000 in additional federal aid is available. With employer reimbursement covering tuition, this $21,000 covers books, fees, and provides budget cushion for the full program duration. Net result: degree completed with positive cash position relative to expenses.

Step 4: Apply GI Bill or Military Benefits

Military benefits typically apply to remaining tuition cost after employer reimbursement and Pell Grant. The Post-9/11 GI Bill specifically pays tuition and fees, so it overlaps with employer reimbursement. Many veterans use GI Bill benefits for the portion of cost above what employer reimbursement covers, allowing them to preserve GI Bill entitlement for future use (graduate school, for example).

For active-duty service members using Military TA, the typical pattern is to use TA for current courses while preserving GI Bill for post-service education. This maximizes total lifetime education benefit.

The Stacking Result

For working adults with moderate income, the four-benefit stack can produce remarkable outcomes:

| Scenario | Total Tuition | Stacked Benefits | Out-of-Pocket |

| No benefits | $42,000 | $0 | $42,000 |

| Employer only ($5,250 × 8 yrs) | $42,000 | $42,000 | $0 |

| Employer + 30 transfer credits | $31,500 | $31,500 | $0 |

| Employer + 60 transfer credits | $21,000 | $21,000 | $0 |

| Employer + Pell + transfer | $31,500 | $31,500 + Pell excess | Negative (gain) |

| Veteran with GI Bill + employer | $42,000 | $42,000+ | Negative (gain) |

Use the calculator at the top of this page to see your specific stacked benefit position based on your employer’s reimbursement amount, your federal aid eligibility, and your transfer credits.

What Employers Actually Offer (Survey of Major U.S. Employers)

Most major U.S. employers offer some form of tuition reimbursement. The specific amounts and structures vary substantially. The table below summarizes representative programs across major industries.

| Employer | Annual Reimbursement | Notable Features |

| Starbucks (College Achievement Plan) | 100% tuition at ASU Online | First fully covered bachelor’s program in retail |

| Amazon (Career Choice) | Up to $5,250 | Prepaid tuition model, no reimbursement delay |

| Walmart (Live Better U) | $1 per day | Effectively full coverage at partner institutions |

| UnitedHealth Group | $5,250 + UAGC partnership | $460/credit reduced rate at UAGC |

| IBM | $5,250 | Plus SkillsBuild free platform, digital credentials |

| Verizon (Lifelong Learning) | Up to $8,000 | Higher than Section 127 cap (taxable above $5,250) |

| Boeing (Learning Together) | Up to $25,000 | Among the most generous in U.S. employers |

| RTX (Employee Scholar Program) | No publicly disclosed cap | Pays directly to institutions |

| Bank of America | Up to $7,500 | Higher than Section 127 cap (taxable above $5,250) |

| JPMorgan Chase | Up to $5,250 | Standard Section 127 cap |

| Target (Education Assistance) | Up to $5,250 + Guild partners | Partner institution discounts |

| Home Depot | Up to $5,000 | Career-focused program selection |

For specific employer program details: Starbucks College Achievement Plan: Full Breakdown for Partners.

For Walmart-specific program details: Walmart Live Better U Explained: Which Online Degrees Are Covered?.

For Amazon-specific program details: Amazon Career Choice: Is It Worth Using for an Online Degree?.

For Target-specific program details: Target Education Assistance: How Guild Education Works for Online Degrees.

For Home Depot-specific program details: Home Depot Tuition Assistance: Best Online Degrees to Use It On.

Strategy for Maximizing Your Stacked Benefit Value

Working adults who get the most from benefit stacking typically follow a coordinated strategy rather than enrolling reactively. Five strategies produce the strongest outcomes.

Strategy 1: Optimize Transfer Credit Before Enrolling

Transfer credit reduces total program cost more efficiently than any single benefit. Before enrolling at any institution, request transcript evaluations from your top three target institutions. The institution with the strongest credit acceptance for your specific prior coursework can save thousands of dollars.

Working adults with substantial industry certifications should specifically target institutions with formal prior learning assessment programs. Purdue Global, Excelsior University, Charter Oak State College, and Thomas Edison State University have particularly strong prior learning assessment infrastructure.

Strategy 2: Select Cost-Competitive Accredited Institutions

Total program cost depends heavily on per-credit pricing. The same employer reimbursement provides 80% to 100% more coverage at affordable institutions ($300-400 per credit) versus premium institutions ($600-900 per credit). For most working adult career trajectories, regional accredited online programs at affordable institutions produce equivalent career outcomes.

For institutions under $300 per credit: Best Online Universities Under $300 Per Credit.

Strong combinations of cost and accreditation include:

Southern New Hampshire University ($330/credit): Southern New Hampshire University Online College Review.

Western Governors University ($4,400 per 6-month term, effectively under $367/credit): Western Governors University Online College Review.

Purdue Global ($371/credit with discounts): Purdue Global Online College Review.

ASU Online (varies by program, $530-$1,000+/credit): ASU Online College Review.

Capella University ($390/credit GuidedPath, $2,500/quarter FlexPath): Capella University Online College Review.

Strategy 3: Pace Coursework to Use the Full Annual Cap

The $5,250 annual cap resets each calendar year. Employees who enroll in 12 to 15 credits per year (at $350-$440 per credit average) capture the full benefit. Employees who enroll in 6 credits per year capture only half. Pacing is the difference between full and partial benefit capture.

Working adults often underestimate how many credits they can complete annually. A standard course load is 3 credits, which typically requires 9-12 hours of study time per week per course over a 16-week term, or 12-18 hours per week over an 8-week accelerated term. Two courses simultaneously (6 credits) is sustainable for most working adults; three courses (9 credits) is achievable with strong scheduling discipline.

Strategy 4: Complete FAFSA Even If You Think You Don’t Qualify

Working adults frequently skip FAFSA based on the assumption that working income disqualifies them from need-based aid. This is often incorrect. FAFSA takes 30 minutes to complete and reveals actual Pell Grant eligibility based on the specific federal formula, which weighs household size, dependents, and other factors beyond gross income.

The cost of completing FAFSA is 30 minutes; the potential benefit is $3,500 to $7,395 per year in tax-free grants. The expected value of attempting FAFSA is positive even if you think you might not qualify.

For complete FAFSA strategy for working adults: FAFSA for Online Students.

Strategy 5: Pre-Approve All Employer Reimbursement

Most employer reimbursement programs require pre-approval before enrollment. The pre-approval process verifies that the institution and program meet employer relevance requirements. Skipping pre-approval is the single most common cause of denied reimbursement after course completion.

Pre-approval should specify the institution, the specific program of study, the total expected cost, and the timeline. For multi-year programs, employees should clarify whether the pre-approval covers the full program or whether re-approval is required annually.

Common Questions About Section 127 Stacking

Can my employer reimburse more than $5,250 per year?

Yes, but amounts above $5,250 in a single calendar year are taxable to the employee. The amount above the cap is added to W-2 income and taxed at the employee’s marginal rate. Some employers (Boeing, Verizon, RTX, Bank of America) explicitly offer above-cap reimbursement; the employee receives the gross amount with corresponding tax liability.

For most employees, the calculation works out favorably even with tax implications. A $10,000 annual reimbursement at a 22% marginal tax rate produces $1,045 in tax on the $4,750 above the cap. Net benefit: $8,955 versus $5,250 capped. The above-cap reimbursement is still worth accepting.

Does Pell Grant affect employer reimbursement?

No. Pell Grant and employer reimbursement apply independently. Pell Grant pays the student directly through the institution; employer reimbursement pays the employee for documented tuition costs. The two benefits can apply to the same tuition cost without conflict. Excess Pell Grant funds (if Pell plus employer exceeds tuition) can be used for books, fees, transportation, and living expenses.

What happens if I leave my employer before completing the degree?

Employer reimbursement typically covers only courses completed while employed. Departing mid-program means losing reimbursement on remaining coursework. Many employers require service commitments (typically 1-2 years of continued employment after substantial reimbursement); employees who leave within the commitment window may be required to repay the benefit.

Pell Grant and GI Bill benefits are not affected by employer departure. Those benefits stay with the student regardless of employment status.

Can I use Section 127 reimbursement at any institution?

Generally yes, at any regionally accredited institution. Some employers restrict reimbursement to specific institutional partnerships (Walmart’s Live Better U specifies partner institutions; Disney Aspire has specific partner universities). For most employers without restrictions, the standard requirement is U.S. regional accreditation and relevance to the employee’s current role or realistic future role.

For accreditation verification: What Makes an Online University Legitimate?.

Does Section 127 apply to certifications and bootcamps?

Section 127 explicitly covers tuition, fees, books, and supplies for both undergraduate and graduate coursework. Industry certifications and bootcamps are not always covered under Section 127 specifically, but many employers reimburse them through separate professional development programs. Verify specific employer policy before assuming coverage.

Can I use the benefit for online programs?

Yes. Section 127 makes no distinction between online and on-campus programs. Online degrees from regionally accredited institutions qualify identically to on-campus degrees. The benefit applies to tuition and fees, which are typically the same or lower for online programs.

Bottom Line: Use the Calculator to See Your Position

Section 127 employer tuition reimbursement, when combined with Pell Grant, GI Bill, and transfer credits, can substantially reduce or eliminate out-of-pocket cost for an online degree. The specific stacked value depends on your individual situation: which employer offers what reimbursement, whether you qualify for federal aid, what military benefits apply, and how many transfer credits your prior coursework or experience produces.

The practical recommendations that emerge from how stacking actually works:

- Calculate your stacked benefit position before selecting an institution; the institutions that produce the strongest outcomes vary based on which benefits you can stack

- Complete FAFSA even if you think you might not qualify for Pell Grant; the cost is low and the potential benefit is substantial

- Optimize transfer credit aggressively before enrolling; industry certifications, military experience, and prior coursework often translate to substantial credit

- Select cost-competitive accredited institutions; the same employer reimbursement covers more of the total cost at affordable institutions

- Pace coursework to use the full annual employer reimbursement cap

- Pre-approve all employer reimbursement before enrolling; this prevents the most common reason employees lose expected benefits

[OPTIONAL SECOND SHORTCODE PLACEMENT: [ct_127_calculator]. Placing the calculator a second time at the end of the article gives readers a strong action point after reading the strategy. Skip if you only want one calculator on the page.]

For the broader foundation on accredited online degrees as an adult learner: The Complete Guide to Earning an Accredited Online Degree as an Adult Learner.

For the broader employer tuition reimbursement framework: Employer Tuition Reimbursement Explained.

For complete adult learner financing strategy: How Adult Students Can Graduate With Minimal Debt.